Documentation Index

Fetch the complete documentation index at: https://docs.fizenfoundation.com/llms.txt

Use this file to discover all available pages before exploring further.

The Trillion-Dollar PayFi Opportunity

Before analyzing competitors, it is crucial to understand the sheer scale of the battlefield. Payment Finance (PayFi) is no longer a niche crypto experiment; it is the most tangible, value-generating sector in Web3, systematically replacing legacy financial rails. According to the 2026 landmark report by McKinsey & Company and Artemis Analytics, the market is shifting rapidly from speculative trading to real-world utility:- The Raw Infrastructure Boom: Raw on-chain stablecoin volume has surged to $35 trillion in early 2026, up from roughly $10.8 trillion in 2023. This represents an explosive 324% growth over just two years, proving that the underlying blockchain infrastructure is now capable of handling global-scale liquidity.

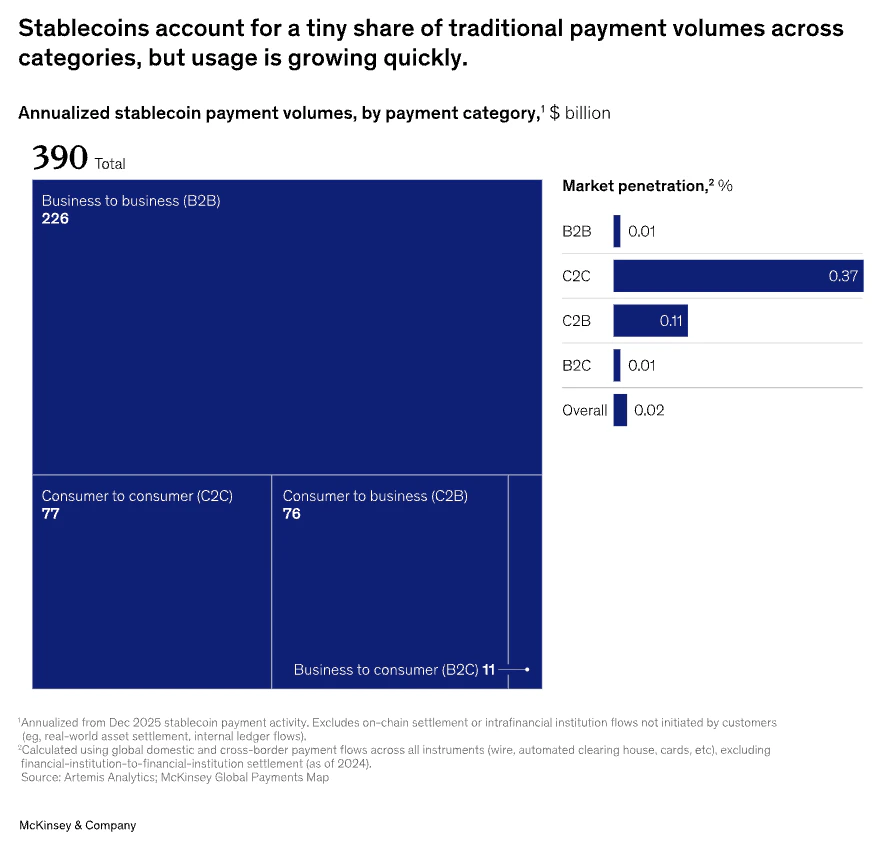

- The Reality of Stablecoin Payments: However, this $35 trillion figure is largely driven by trading and bots. The true “actual payments” volume is $390 billion. Most importantly, this real payment activity is dominated by the B2B sector, which reached $226 billion (a staggering 733% YoY growth). Within this, consumer use cases are rapidly maturing, representing nearly $100 billion in annual real-world utility (driven primarily by $90 billion in remittances/payroll and rapidly expanding card-linked spending), proving that everyday users are successfully bypassing traditional banking.

- The Massive Untapped TAM: Despite this momentum, the $390 billion in stablecoin payments has barely scratched the surface, penetrating just 0.02% of the global payments market. The infrastructure is proven, the retail demand is surging, but the window to capture the remaining 99.98% of everyday commerce is closing fast.

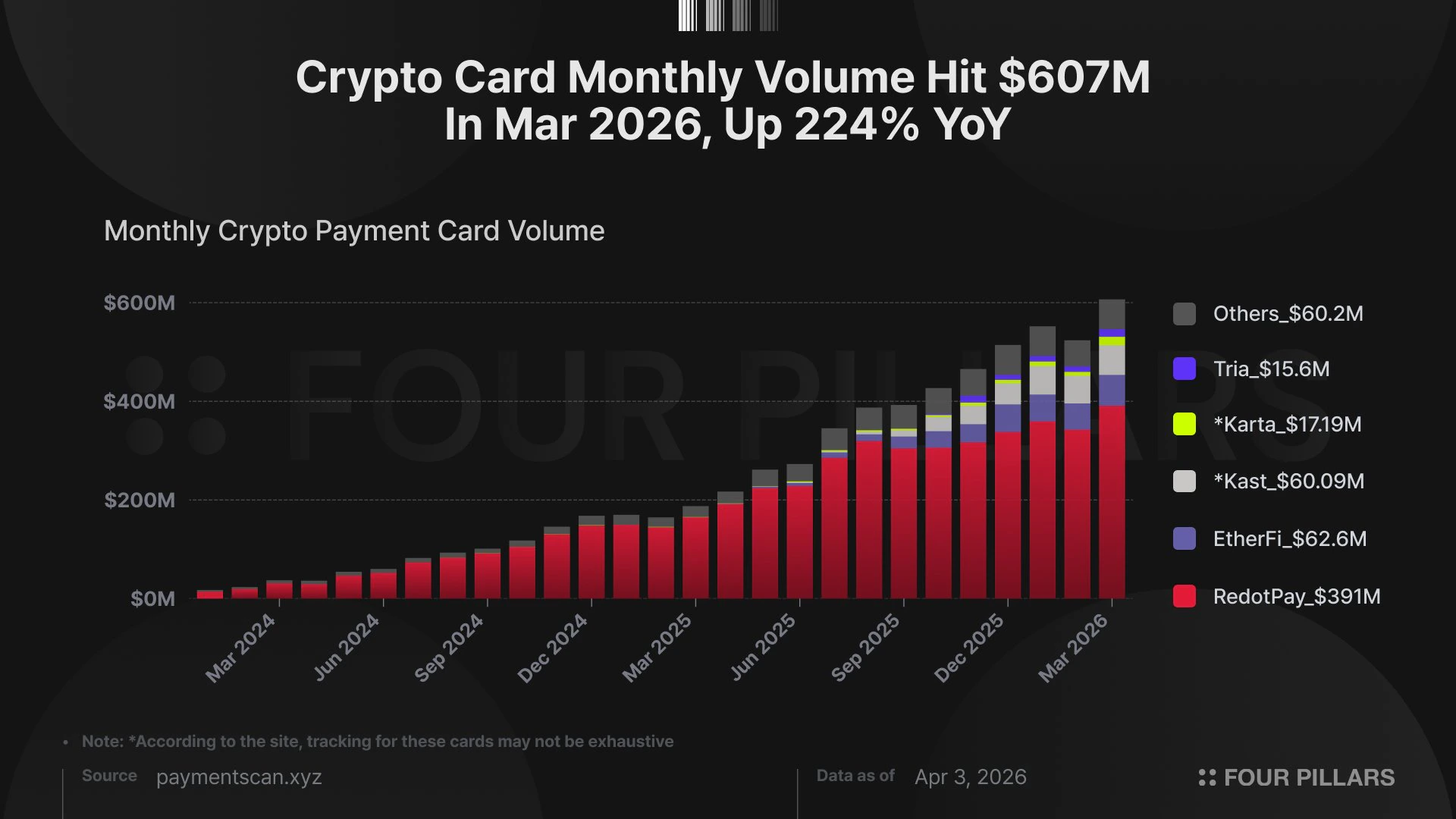

- Crypto Card Hypergrowth (B2C): On the consumer side, monthly crypto card transaction volumes have skyrocketed to over $607 million, representing a massive 224% YoY growth.

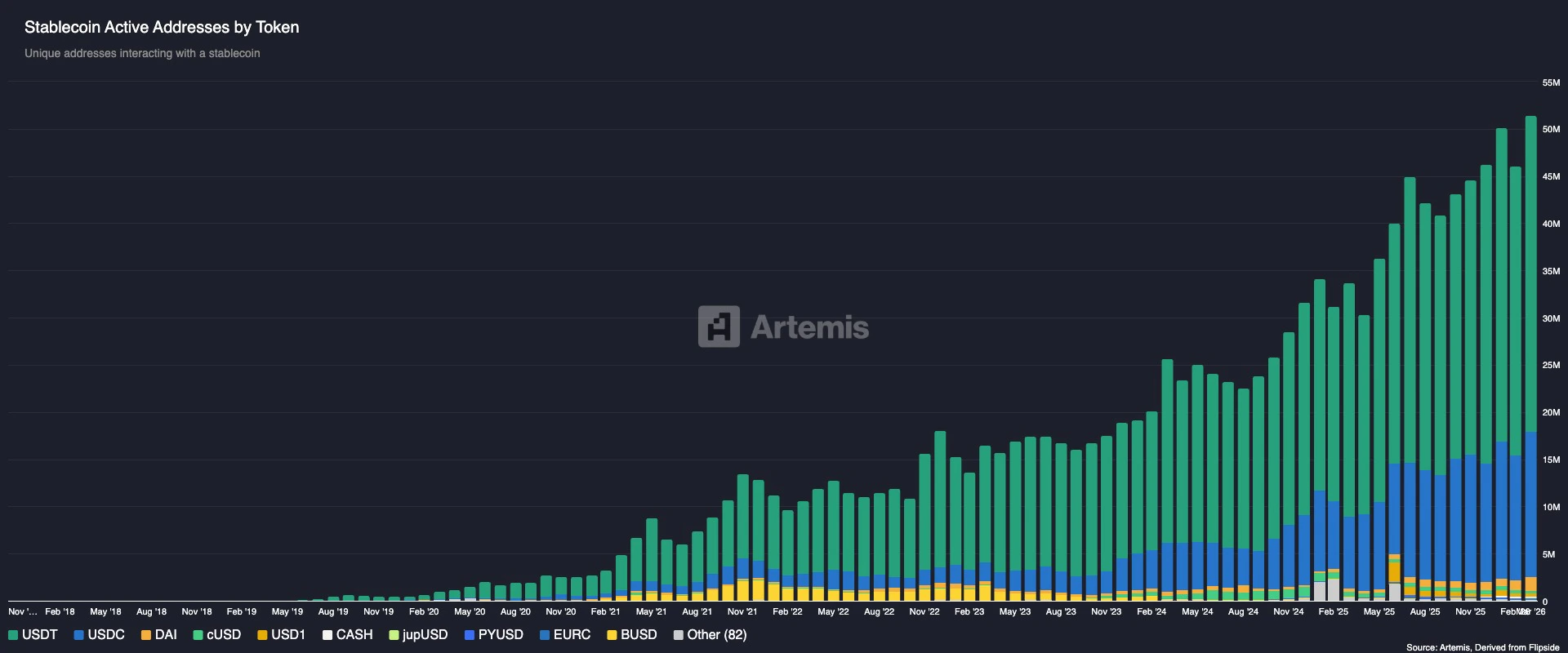

- The 50 Million User Opportunity: Volume is only half the story. As of Q1 2026, monthly active stablecoin addresses have surged past 50 million. To put this in perspective, this number was less than 1 million in early 2020—representing a 5,000% growth over six years. This is a massive, hyper-growing retail base holding digital dollars, yet they remain trapped by friction—unable to easily book a flight or pay for daily goods without complex, high-fee off-ramps. Fizen is built to directly unleash the spending power of these 50 million users.

TAM, SAM, SOM

For investors, the math behind Fizen’s trajectory is remarkably straightforward. We are not creating a new behavioral paradigm; we are capturing an existing, massive migration of capital.- TAM (Total Addressable Market) - The Legacy Giant: The global traditional payments market sits at an astronomical $1.6 Quadrillion. This is the ultimate ceiling that PayFi is slowly absorbing.

- SAM (Serviceable Available Market) - The Proven Crypto Reality: $390 Billion in actual annual stablecoin payments and a rapidly growing base of 50 Million monthly active users. This is the market that has already crossed the chasm. They hold crypto, they want to spend it, and they represent both massive B2C (consumer lifestyle/remittance) and B2B demand.

- SOM (Serviceable Obtainable Market) - The Fizen Target: Fizen’s dual-engine strategy is what sets it apart. While competitors focus solely on single-use B2C cards, Fizen attacks the market with both a Consumer Super App (B2C) and a powerful Merchant Gateway (Fizen Pay - B2B). By capturing just 1% of the current $390B SAM, Fizen will process $3.9B annually.

The Current Market Contenders

1. Legacy Giants (Crypto.com, Wirex)

- The Flaw: They offer high cashback (up to 8%), but these rewards are paid out in highly inflationary ecosystem tokens. Users are forced to stake massive amounts of capital, only to watch the token value plummet as the protocol endlessly prints new tokens to fund the rewards.

- Market Position: They have strong brand awareness but suffer from unsustainable tokenomics that eventually alienate their user base. Furthermore, they are strictly B2C, ignoring the B2B market entirely.

2. Pure Card Gateways & Infrastructure (RedotPay, Reap, Kast, Rain)

- The B2B Illusion: While platforms like RedotPay report massive volumes (approx. $391M/month), it is crucial to understand that much of this is aggregated B2B volume from various white-label partners. They operate primarily as backend payment gateways bridging crypto wallets and Visa/Mastercard.

- No Yield, No Ecosystem: As standalone B2C apps, they are functionally sound but one-dimensional. User funds sitting in these apps remain idle (generating zero yield), and they lack native ecosystems, forcing users to leave the app to book flights, buy goods, or manage travel.

- Fizen’s Strategic Play (Commoditizing the Backend): Fizen does not need to reinvent the wheel. Fizen can seamlessly utilize these very platforms as backend infrastructure providers while completely dominating the B2C consumer layer and providing a direct B2B payment gateway (Fizen Pay). By layering Real Yield, an expansive lifestyle ecosystem, QR payments, and AI Agents on top of their payment rails, Fizen captures the actual end-users and their long-term loyalty. This turns perceived competitors into mere utility pipes for the Fizen Super App.

The Fizen Super App Advantage

Fizen is built to be the ultimate Crypto Neobank, structurally designed to outcompete and absorb the user bases of the platforms above across five key vectors:- Omnichannel Payments (Cards + QR Codes + B2B): While competitors rely solely on Visa/Mastercard networks for retail, Fizen integrates Local QR Code Scanning for emerging markets and Fizen Pay for B2B e-commerce settlements. Fizen captures the full spectrum of the $390B real-payment market.

- Massive Built-in Inventory: Fizen is a lifestyle hub. Users can directly book hotels, buy flights, purchase global eSIMs, and access over 21,000 products from 2,500+ brands without ever leaving the app. This creates unparalleled stickiness.

- The Foundation for AI Agents: This rich, native inventory is not just for human convenience—it is the critical infrastructure required for Fizen’s future roadmap as an Autonomous AI Personal Assistant. While competitors remain “dumb payment pipes,” Fizen will allow users to command AI to autonomously book travel and execute crypto payments in the background.

- Sustainable, Unbeatable Rewards: To rapidly acquire users from giants like RedotPay and Crypto.com, Fizen offers top-tier cashback. However, instead of printing inflationary tokens, Fizen funds these rewards using Real Yield generated by the 3e5.ai institutional treasury. This ensures a permanent, sustainable user acquisition loop.

- TradFi-Grade Luxury & HNWI Perks: While legacy crypto cards offer basic airport lounge access at best, Fizen elevates PayFi to private banking standards. High-volume users and large $FIZEN stakers unlock the Fizen Elite Tier, gaining access to bespoke global concierge services, invite-only deals, and a private networking circle. This not only attracts traditional High-Net-Worth Individuals (HNWIs) into Web3 but transforms the $FIZEN token into a coveted Status Symbol.